Abstract 2013 is a key year for China's equipment industry to implement the “Twelfth Five-Year Planâ€. The domestic and international environment faced by the industry has been relatively improved, and the economic operation has shown a steady development. However, the complicated situation has not changed fundamentally. exhibition...

The year 2013 is a crucial year for China's equipment industry to implement the “Twelfth Five-Year Planâ€. The domestic and international environment faced by the industry has been relatively improved, and the economic operation has shown a steady development. However, the complicated situation has not changed fundamentally. Looking forward to 2014, China's equipment industry development opportunities and challenges coexist, not only the transformation and upgrading, the new round of reform policy measures introduced the release of development dividends, the domestic economy tends to pick up and other favorable factors, but also the international market demand continues to be weak, corporate production cost pressure Increase the disadvantages. I. Basic judgment on the situation in 2014

(1) The growth rate of production and exports is rising slowly

Since 2013, there have been signs of recovery in the world economy, but the old risks overlap with the new disturbances, and the road to recovery is still bumpy. Under the effect of a series of national policies of steady growth, restructuring, and reform, the domestic economy continued to stabilize and rebound. Affected by the comprehensive economic situation at home and abroad, China's equipment industry's domestic demand has picked up, and the growth rate has slowly increased. From January to September, the industrial added value of equipment manufacturing enterprises above designated size increased by 9.9% year-on-year (up 9% in the first quarter and 9.2% in the second quarter), with 12.8% in the month of September. Affected by factors such as the decline in the growth rate of fixed investment in the equipment industry and the continued increase in operating costs, the equipment industry will maintain a “stable†trend in 2013, and the chances of a strong recovery will be small. On the export side, the monthly growth rate of export delivery value has rebounded since August. It is expected that the export situation in the fourth quarter will remain in the first three quarters, and the growth rate of export delivery value will increase slowly.

It is expected that in 2014, China's equipment industry will still face a more complicated development situation. The macro economy will still be in the austerity stage after the “4 trillion†investment brings a period of high growth. The task of “de-capacity and defoaming†will still take some time to complete, and domestic demand for equipment products will not increase significantly. However, due to the impact of the new round of reform policy measures to release the development dividend, the equipment industry will sprout new power and growth points, such as rail transit equipment will enter a period of rapid growth. Under the influence of the above factors, China's equipment industry will continue to develop steadily in 2014, and the annual growth rate of industrial added value is expected to remain at around 13%.

(II) Accelerating the pace of transformation and upgrading of the equipment industry

In 2013, from the perspective of the domestic environment, when the equipment industry faced many difficulties such as sluggish domestic demand and weak export growth, various problems and contradictions concealed by high-speed growth were successively exposed. In the past, relying on demographic dividends and sacrificing the environment, The extensive economic growth model driven by investment is unsustainable. Demand upgrading and fierce market competition have brought about newer, higher and more urgent requirements for structural adjustment, transformation and upgrading of the whole industry. Therefore, under the influence of the market reversal mechanism, more and more equipment manufacturing enterprises have strengthened innovation and transformation and upgrading. Among the 80 national technological innovation demonstration enterprises announced by the Ministry of Industry and Information Technology in September, equipment manufacturing enterprises accounted for half, compared with 10 new ones last year.

It is expected that in 2014, under the background of the implementation of the “Industrial Transformation and Upgrading Plan†and the “Strategic Emerging Industry Development Planâ€, under the downward mechanism of domestic and international demand upgrading, equipment industry enterprises will further improve production efficiency and reduce resources. Consumption. In view of the fact that the profit rate of the equipment industry is still in a downward trend, it has not really got rid of the predicament and entered the track of sound development. Therefore, the equipment industry needs to make more efforts in adjusting the structure and strengthening management. Moreover, under the guidance of national policies, industries such as agricultural machinery, intelligent instrumentation, and other industries closely related to consumption, informatization, and automation will develop faster than the typical investment products industry, and the future structural adjustment direction of the equipment industry will be more focused and adapted. This trend of change.

(III) Continuous growth of production and sales of the automobile industry

Since 2013, driven by urbanization and the increase in the income and consumption levels of residents in villages and towns, passenger cars have experienced different levels of sales. From January to October, the production and sales of automobiles were 17.8544 million and 17.815.58 million, respectively, up 13.6% and 13.5% year-on-year. The annual growth rate of automobile production and sales is expected to reach 17% and 15% respectively, and with the "continuation of new energy vehicles" The implementation of the Notice on Promoting Application Work, the sales of new energy vehicles are expected to grow.

It is expected that in 2014, China will carry out reforms in the access of the automobile industry. If the “investment of foreign capital and domestic car companies cannot exceed two, and the ratio of joint venture shares cannot exceed 50%â€, the investment access policy will be open to the market. Great changes will occur. In terms of market demand, with the implementation of the central government's investment of 4 billion yuan in subsidies for the promotion of new energy vehicles, the production and sales of new energy vehicles will see rapid growth in 2014. At the same time, with the introduction of a series of government pollution control measures such as the Air Pollution Prevention Action Plan and the increasing awareness of environmental protection, the small car market will usher in new opportunities for development. However, in 2014, the auto industry will also face the downward pressure on economic growth caused by macroeconomic restructuring, as well as the adverse impact of government restrictions on purchases and restrictions. It is expected that the growth rate of China's automobile production and sales will be basically the same as that in 2013, and the growth rate of production and sales will be achieved. At around 15%.

(4) Moderate growth in production and sales of machinery industry

Since 2013, the machinery industry has continued to maintain a stable development trend. The main economic indicators have grown moderately. From January to September, the growth rate of production and sales has increased by nearly 3 percentage points over the previous year. The profit growth rate has increased by 7 percentage points over the previous year. The speed is faster than the production and sales, the industry's rebound is stronger than the national industry, showing that the industry boom is slowly picking up. Industries related to the construction of iron-based buildings, the development of new urbanization and the construction of “smart citiesâ€, such as elevators, urban rail equipment, smart grids, Internet of Things equipment, agricultural machinery and other industries have achieved rapid growth, environmental protection equipment, intelligent equipment such as Industrial robots and the 3D printing industry have become new growth points, but the output of typical investment products such as power generation equipment, machine tools, and construction machinery continues to decline.

It is expected that in 2014, the demand for mechanical equipment will continue to heat up due to the improvement of the economic environment, the introduction of the “New Urbanization Plan†and the construction of “smart citiesâ€. However, due to the unfavorable factors such as the decline in the growth rate of fixed investment in the machinery industry and the continued increase in operating costs, the operation of the machinery industry will continue to maintain a steady state. The probability of a strong recovery is not large. The growth rate of production and sales is expected to be around 14%. From the perspective of sub-sectors, conventional power generation equipment and power transmission and transformation equipment, metallurgical mining equipment, heavy machinery, general machine tools and other industries will continue to be in a state of sluggish demand; demand for high-end machine tools, robots and automatic production lines will rise; the construction machinery market will gradually increase from big ups and downs. Returning to normal; the growth rate of agricultural machinery production and sales will gradually decline, but the large-scale high-end agricultural machinery products market will continue to produce and sell.

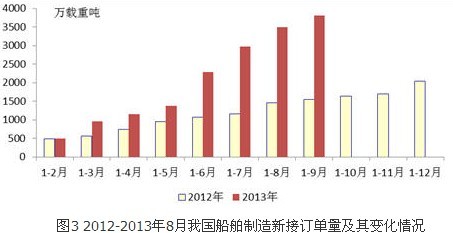

(5) The shipbuilding industry is expected to bottom out

In 2013, under the influence of the weak global economic recovery and the sluggish global shipping market, the main operational indicators such as shipbuilding completion volume, hand-held orders, economic benefits and exports all showed a downward trend. However, the volume of new orders for ships has rebounded sharply, marking the bottoming out of the shipbuilding industry. From January to September, the country's new orders for ships were 38.06 million DWT, up 147.1% year-on-year. The fourth quarter will continue the trend of the first three quarters. It is estimated that the annual shipbuilding completion will be around 45 million tons, and the new ship orders will also grow. The situation can reach 45-50 million tons.

It is expected that in 2014, with the recovery of the world economy, the shipbuilding industry will usher in a new round of recovery based on the application of new technologies and the development of new ship types. Along with the introduction of a series of new standards and new norms of the International Maritime Organization, such as the new energy efficiency design index (EEDI) put forward higher requirements for ship energy efficiency and emissions, the future hull design and manufacturing will become a major trend in the direction of energy conservation and emission reduction. In China, the State Council recently issued the “Implementation Plan for Accelerating Structural Adjustment and Promoting Transformation and Upgrading of Shipbuilding Industry (2013-2015)†to clarify seven major tasks, and will also greatly accelerate the shipbuilding industry to resolve overcapacity, adjust industrial structure, and accelerate transformation and upgrading. At the pace, some companies with weak R&D capabilities and slow transitions will be eliminated. At the same time, due to the development of marine engineering and other industries, the demand for the ship market will show structural changes. LNG ships and energy-saving and environmentally-friendly ships and special ships, ocean-going fishing boats, fishery vessels, coastal and inland rivers will have a certain scale. Demand. In summary, in 2014, China's shipbuilding industry will bottom out, and the three major indicators will increase.

(6) The rapid development of intelligent manufacturing equipment industry

In 2013, economic restructuring and rising labor costs continued to drive the upgrading of the manufacturing industry, and the demand for smart manufacturing equipment was strong. A series of policies to promote the intelligent manufacturing equipment industry have been continuously introduced, such as “specialized development of intelligent manufacturing equipment†and “Guidance on promoting the development of industrial robot industryâ€. The cumulative effect of the implementation of policies has been increasing, driving industrial robots and high-end CNC machine tools. The rapid development of industries such as intelligent instrumentation and intelligent major complete sets of equipment has brought the industrialization level of intelligent manufacturing equipment to a new level.

It is expected that in 2014, a new round of technological revolution represented by cloud computing, artificial intelligence, 3D printing, etc. will accelerate development, and the acceleration of industrial structure adjustment and upgrading will increase the demand for intelligent manufacturing equipment. It shows a rapid expansion. From the perspective of the development of sub-industries, with the increase in the development of special planning cities for smart city development, equipment related to smart city construction, such as Internet of Things equipment and intelligent transportation equipment, will usher in rapid development. In addition, the smart grid will complete the process of demonstration, technology unification and planning and formulation in 2013. It will enter full promotion in 2014, and the smart grid equipment industry will also enter a rapid development channel.

Second, several issues that need attention

(1) The operating pressure of enterprises is still relatively large

First, due to the lack of market demand and homogenization competition, the phenomenon of blindly grabbing orders has occurred from time to time. In 2014, the price of equipment products will continue to run at a low level since 2012, and the price index for the month will still show a slight downward trend. Second, as the economy recovers, the purchase price of fuel and power transportation will increase, and the procurement cost of equipment industry will also rise slowly. Third, with the financial reforms and the attention of banks to equipment industry enterprises, the financing environment of large enterprises will improve, and the financial expenses and interest expenses will fall back from 2013, but the large and medium-sized enterprises will still face Difficulties in financing and high financing costs. Fourth, due to the transformation of economic growth mode, energy resources and environmental protection costs will continue to rise. Therefore, in 2014, China's equipment industry under the "double squeeze" of high operating costs and product prices, the pressure on production and operation of enterprises is still relatively large.

(2) The export situation is still difficult to be positive and optimistic

In 2013, under the background of the slowdown of the world economic recovery, the promotion of the “re-industrialization†strategy of the western developed countries, and the increasingly fierce competition in the international market, although China’s equipment industry has certain international comparative advantages, the rapid growth of exports that has continued for many years has begun to cause increasingly The trade environment is still worsening due to fierce trade frictions. Therefore, although the year-on-year growth rate of export delivery value for the two consecutive months in August and September decreased from negative to positive, increasing by 2.25% and 3.36% respectively, the cumulative increase in the first three quarters was still 1.55% lower than the national foreign trade level ( 8%).

In 2014, as the international economic recovery road is still tortuous, the international market demand is still weak overall, the competition among industries in various countries is increasingly fierce, and the trade friction situation is still grim. The difficulties and risks faced by China's equipment industry products are still relatively high. However, under the background of a series of national policies and measures to promote foreign trade development, the level of export trade facilitation of China's equipment industry will continue to improve. At the same time, many enterprises will actively transform and upgrade, and new export competitive advantages will continue to emerge. It is expected that China's equipment industry will be in 2014. Product exports may be slightly better than in 2013.

(3) Insufficient technology investment is still a major obstacle to innovation

Entering 2014, China's equipment industry will still have insufficient technical input level, which has become a major obstacle to China's independent development of core or key technical capabilities. First, the investment intensity of R&D activities of enterprises is still low. In recent years, it has been hovering around the low range of about 2%. Compared with the level of 4%-5% in developed countries, there is still a big gap, which cannot provide strong innovation for independent innovation. Support. Second, the R&D investment is scattered. Most R&D investment is in the development of tracking imitation or supporting technology, and the investment in basic technology for the industry is seriously insufficient. Third, the average possession of scientific and technological personnel in the equipment industry is still low. The proportion of scientific and technological personnel in the equipment industry is relatively low, only about 3%, which is lower than the level of more than 5% in industrialized countries.

(4) The problem of structural overcapacity in some industries

At present, the problem of overcapacity in the traditional industries of the domestic equipment industry is still outstanding. First, the general-purpose low-end equipment is seriously oversupplied. The R&D and manufacturing capabilities of medium and high-end equipment have not been significantly improved, and the supply capacity is seriously insufficient. A large number of high-end equipment orders, including the domestic market, are monopolized by foreign manufacturers. For example, the shipbuilding type built by China's shipbuilding enterprises is mainly based on low-value-added ships such as oil tankers and bulk carriers, and the construction capacity of high-value-added ships such as large container ships, liquefied natural gas ships and offshore engineering equipment is insufficient. Second, the phenomenon of homogenization of products is serious, and it is not suitable for the market demand for transformation and upgrading of downstream industries. In recent years, relying on investing in high-speed engineering machinery, power transmission and transformation equipment, wind power equipment, machine tools and other industries, with the accelerated upgrading of equipment industry users, competition with price wars is difficult to meet the requirements of users for product precision, green and intelligent. And the ability to provide a total solution capability for the business. It is expected that in 2014, the structural overcapacity of China's low-end machine tools, wind power equipment, construction machinery and ships will continue to exist, and the pressure on industrial restructuring will be further increased.

Third, the countermeasures should be taken

(1) Enhance the technological level of enterprises and accelerate the pace of industrial upgrading

First, through various forms of centralized funds, focus on supporting the major commonalities and key technologies of the equipment industry, and focus on supporting the use of high-tech transformation to upgrade traditional industries. The second is to support enterprises to dock the international industrial chain, and guide qualified enterprises to acquire overseas famous enterprises, R&D institutions and marketing networks. The third is to promote the construction of a number of major projects, set up special funds to support, provide green channels and other guidance to the development of enterprises, and actively promote the healthy development of new industrial projects such as CNC machine tools, industrial robots, 3D printing, etc., with the project to promote the core capabilities of enterprises.

(2) Taking multiple measures to actively expand the export of equipment products

First, improve the export tax rebate policy, appropriately increase the export tax rebate rate for some high-tech, high value-added equipment products, and provide a strong foreign trade financial environment for equipment manufacturing export enterprises. Second, encourage financial institutions to increase the export of export credit funds, and support domestic enterprises to undertake major foreign projects, thereby driving the export of complete sets of equipment and construction machinery. The third is to guide equipment manufacturing enterprises to adapt to changes in international market demand, adjust and optimize the structure of export products according to user needs, and gradually reduce the export of “two high and one capital†products. Fourth, encourage enterprises to actively explore the Middle East, Central Asia, Latin America, Africa, India, Brazil, Russia and other markets, and promote the diversification of export markets to make up for lost shares in the EU, the United States and other markets.

(3) Build an innovation system and enhance the ability of independent innovation

First, aiming at the weak links of key core technologies, basic technologies and process technologies, giving full play to the role of national key laboratories, national engineering technology research centers, and key institutions such as industry key laboratories and engineering technology research centers, and taking effective measures to strengthen the industry. The research and input of common technology promotes the transformation and application of scientific and technological achievements. The second is to promote large enterprises (groups) and large and medium-sized enterprises to establish key enterprise laboratories, technology centers and research and development institutions, and to form a product technology development and innovation system based on enterprises, in some key areas, key industries, key products and key processes. Improve the independent innovation capability of enterprises. The third is to establish a diversified, multi-channel, multi-level independent innovation infrastructure capacity investment and financing system, give play to the guiding role of fiscal investment, and explore the establishment of government funds to guide the social capital investment mechanism.

(4) Vigorously promote energy conservation, emission reduction, green manufacturing, etc.

First, energy conservation and emission reduction, green manufacturing and basic work are the focus of transformation and upgrading. Second, continue to strengthen the revision and revision of new products, energy-saving and high-efficiency products, improve processes, transform backward equipment, and promote the use of energy-saving and emission-reducing equipment. The third is to speed up the research and development of high-efficiency energy-saving technologies and equipment, develop major equipment represented by large-scale and high-efficiency power generation equipment, research and develop and promote a wide range of general-purpose energy-saving mechanical and electrical products represented by high-efficiency motors and energy-saving transformers, and promote development. Special energy-saving devices represented by energy recovery devices such as residual heat and residual pressure.

Isuzu Supply Module,Isuzu Supply Module 8982264733,ISUZU Injector,ISUZU 4HG1 Injector

JINING SHANTE SONGZHENG CONSTRUCTION MACHINERY CO.LTD , https://www.sdkomatsugenuineparts.com