According to the monthly small sample statistical report of the club, the average sales revenue in January-April decreased by more than 12% compared with the same period of last year; the large sample statistics in the first quarter showed a year-on-year decline of 9%. There is no sign of a steady decline, and the situation is very serious.

According to the sales information feedback from the tool companies, from the fourth quarter of 2014, the overcapacity pressure accumulated by the manufacturing industry has rapidly increased, and the government's steady growth measures – that is, the previous stimulus measures – have rapidly declined. After entering 2015, the situation has become more serious, which has led to a significant deterioration in the tool sales situation. Specifically, the proportion of enterprises that have achieved sales growth against the trend has increased from more than two-thirds in 2014 to less than one-third (according to the quarterly statistics of the club). The main economic indicators of the industry in 2015 were: the total consumption of the tool market decreased by 9.6% to 31.2 billion yuan (RMB, the same below); the domestic tool share was 19.6 billion yuan, down 11.3% year-on-year; the imported tool was 11.6 billion yuan, down 6.5% year-on-year. Tool exports were 7.6 billion yuan, down 2.6% year-on-year (see Figures 1, 2 and 3, respectively).

Looking back at the development of the tool industry during the “Twelfth Five-Year Plan†period, compared with the sustained rapid development of the previous five-year planning period, it can be said that it is ups and downs, complicated and changeable, and the uncertain factors have greatly increased. This form of development has been deeply imprinted by the continued impact of the global financial crisis on the manufacturing industry – the slow recovery and ups and downs. For China's tool market, in this post-financial crisis period, an extra shock wave has been added. That is, the so-called “four trillion strong stimulus†growth measures introduced by the government at the time, this strong stimulus immediately contributed to China's manufacturing industry formed a rapid V-shaped rebound, reaching its peak in 2011. Under this influence, the domestic cutting tool market has also set a historical record of 40 billion yuan, which is more than 6 billion US dollars according to the exchange rate at that time. It is more expensive than the most powerful European, American and Japanese countries in the global manufacturing industry. 50%, ranking first in the world. Against the background of the slow recovery of the manufacturing market in developed countries at that time, China's tool market rebounded rapidly and became a dazzling bright spot, attracting European, American and Japanese multinational tool companies to substantially increase their investment in China, including the construction of new production facilities. Increase sales outlets, open technical demonstration centers, etc., claiming to achieve the goal of doubling sales in China within three to five years. This new development has laid the foundation for the fierce competition in the domestic tool market after the economic downturn. It is now clear that artificially strong incentives, in addition to bringing instant surprises and short-lived feasts to the domestic tool market, the negative impact is very serious. So far, China's tool companies are still paying for the sequelae of this strong stimulus.

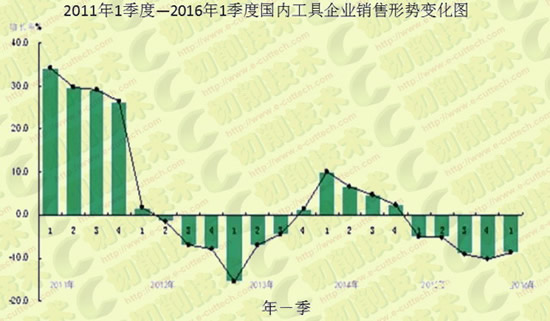

It can be seen from Figure 4 that under the strong stimulus, China's tool market sales revenue peaked in 2011. Later, due to overheated economy and high inflation, the country turned to a tight monetary policy, and the market situation was completely reversed. Up to double-digit negative growth. Although this chart reflects the comprehensive sales situation of the tool industry, in the composition of products and services of tool companies in China, cutting tools account for more than 85%, so this comprehensive chart basically reflects the trend of the tool market. . It can be clearly seen in conjunction with Figure 1 and Figure 4 that the two trends are basically the same. After the domestic tool market reached a peak of 40 billion yuan in 2011, the total trend has been declining all the way to this year. Although there has been a slight rebound in the middle of 2013-2014 under the government's “directional micro-stimulus†(more on this below). Explain that this rebound is also closely related to the efforts of tool companies to accelerate structural reforms. However, this short-lived rebound has not withstood the huge impact of the rapid decline in China's total economic demand. It is worth noting that this runs counter to the gradual recovery of global manufacturing.

It can be seen from the above phenomenon that the economic recovery of developed countries relies on market forces, although it is slow but not ups and downs. In China, there is direct and strong intervention by the government, and different results have emerged. The profound lesson brought about by the ups and downs of the situation in China's tool market is that the government has been involved too much and the market has been distorted. Although the short-term effect is obvious, the consequences are serious, which undermines the endogenous driving force for sustainable economic development.

Promoting the structural reform of the supply side is the economic governance prescription chosen by the central government after repeated exploration and summarization and correct understanding of the economic situation after China's economic development enters a new stage.

In recent years, everyone has an inextricable question: Why is the trend of China's macroeconomic growth rate declining not effectively prevented? In fact, this question is not immediately available to find the correct answer. In recent years, the new central leadership collective has been groping in practice, that is, to solve the problem of how to look at the economic situation and how to do it. From the "three-phase superposition" to the "new normal" to the "supply-side structural reform" is a process of continuous exploration and deepening of understanding. It is now clear that the promotion of structural reforms on the supply side is the trend of the times and the situation. This is the economic governance prescription chosen by the central government after correctly understanding the economic situation.

The economics circles pointed out that reviewing the development of these years has taken some detours. The main reason is that governments at all levels and enterprises have not been able to recognize and grasp the development law of the new normal in time. In the past 30 years of reform and opening up, China's economy has caught up with the globalization of the downwind express, and it has developed too smoothly (although it has paid a heavy price for resources, environment and society). Today, this extensive and rapid development path cannot go on. However, in the early economic development, the inertia formed in the depth of consciousness is not easy to change, so that after the economy enters the new normal, there is no timely change and preparation in terms of concepts and measures.

The new central leadership collective also has a process of deepening understanding through the practice of the economic situation. When they took office, they have already seen the sequelae of strong incentives used by the previous government: the phenomenon of “unstable, unbalanced, uncoordinated and unsustainable†has appeared in economic and social development. Therefore, it is proposed to restart the reform and restore the endogenous power of economic development. Subsequently, the Third Plenary Session of the 18th Central Committee adopted a decision on comprehensively deepening several major issues of reform, and firmly launched the most comprehensive and perfect reform top-level design in history. The reforms that have been stagnant for ten years in China have been restarted and solemnly announced The decisive role of the market in resource allocation. The whole country is excited and won high international praise! Regarding the policy orientation of China's new government governance economy, Barclays Bank of the United Kingdom used "Like Keqiang Economics" to summarize it as a three-fold interpretation of "no stimulation, deleveraging and reform." Although this interpretation is not very accurate, it reflects the expectation that the Chinese economy will embark on the path of transformation and upgrading. In short, the current government has a good start. However, the subsequent operation shows that the road to economic transformation and upgrading is far from smooth, full of contradictions, resistance and even struggle. It was originally thought that through a series of combination exercises such as decentralization and decentralization, decentralization and approval, opening up to the outside world, lowering the entry barriers of some industries, and vigorously promoting fiscal and taxation and financial system reform, it will further mobilize all positive factors and greatly release The development potential, thus changing the old government to replace the old, through the money to force the old routines to stimulate the economy. However, after several years of practice, these reform measures that seem to release economic vitality are far from the original goal, and even can be said to have little effect - the momentum of the decline in economic growth has increased.

Especially in the last two years, under the pressure of continued economic downturn, the government was forced to focus its economic work on stabilizing growth so as to keep the economic growth rate within a reasonable range and prevent a hard landing, in order to create deeper reforms. Necessary conditions. This kind of vision and willingness is of course good, but the reality is cruel. Roots After the international financial crisis, China's economic development momentum has emerged in a grim situation: the development momentum of the troika with the export-oriented main axis has rapidly declined, and the endogenous power of independent innovation is far from being formed. Forcing the government to re-enable the old routine of investment stimulus in order to stabilize growth. In the past few years, the policy orientation has never been stimulating, to micro-stimulus, to directional stimulation, and finally from the end of last year to the beginning of this year, in fact, there has been a strong flood of water flooding. According to the published data: Compared with the “four trillion strong stimulus†period, the new credit of 4.6 trillion in the first quarter of this year was the same as that in the first quarter of 2009, and the total new social financing reached 6.5 trillion, more than 2009. 4.7 trillion in the first quarter. Obviously this is contrary to the goal of reform, which is what everyone does not want to see. Some economists believe that the deeper reason for this step is that the government faces a dilemma between steady growth and reform: if the reform is too strong, the long-term accumulated contradictions will quickly detonate, and the economy will have a hard landing. It is unbearable for China and the world. On the other hand, if we continue to expand our investment to maintain economic growth, the marginal effect of investment is declining. Overcapacity, increased inventories, and increased leverage are accumulating. The accumulated financial risks are increasing day by day, and sooner or later. Even if there is no crisis, another possible consequence is that the company’s overburdened debt will have a long-term, Japanese-like growth that has continued for several years or even decades. It is precisely because of this complicated situation that the government is swinging and swaying in the macro policy orientation. However, other economists disagree with this view, pointing out that the so-called dilemma is only an excuse for the debt-ridden local governments and overcapacity state-owned enterprises to avoid reforms. They pointed out that the data for the first quarter of this year showed that both local governments and state-owned enterprises are adding investment, and banks are also desperately lending. For example, the growth rate of private fixed-asset investment in the first quarter is only 5.7%, while the investment in fixed assets of state-owned enterprises increases. The speed reached 22%. In terms of disposing of overcapacity bots, there is no reduction. Instead, it is expected to reduce leverage by expanding investment to become a large denominator (asset). This kind of practice runs counter to the big policy of the same structure, which is very dangerous! Therefore, the only way out for solving the current economic difficulties in China is to resolutely restart the reforms and speed up the pace of structural adjustment. Macroeconomic policies cannot be left to look forward to the future. .

The debate on the dilemma of steady growth and structural adjustment made a clear and unambiguous conclusion on May 9 this year by the central "authorities" through the People's Daily. The core idea can be attributed to the following passage: The current steady growth, although it still depends on investment, but to grasp the "degree", the most dangerous is to unrealistically pursue "the best of both worlds." At all times, we must put the reform and adjustment structure in the first place.

I believe that the majority of the industry will definitely study this "authoritative person" talk, and do not make more interpretation here. Only extract a few words that are crucial to the future development of the major policy, and share with you:

"Promoting the supply-side structural reform is the main line of China's economic work at present and in the future. Looking at the distance, it is also our "lifeline" that spans the middle-income trap, and it is a war that cannot be lost."

"China's economic operation cannot be U-shaped, it is more likely to be V-type, but the trend of L-type. This L-type is a stage, not one or two years."

The "authoritative person" has promoted the structural reform of the supply side to the current and future period of the main line of China's economic work, and has far-reaching strategic guiding significance for the development of our various industries. This is the major achievement of the new central leadership collective in the practice of summing up and sublimating, from the "three-phase superposition" to the "new normal" to the "supply-side structural reform", after a process of continuous exploration and deepening understanding. The results have comprehensively solved the problem of “how to see and how to do†for the current economy. It will effectively guide the correct direction of China's economic development towards long-term stability.

Now return to our tool industry. In the past few years, the vast number of tool companies have experienced the ups and downs of the domestic tool market. They also deeply understand that in the face of new challenges under the new normal, the best response measures are to adjust the structure and promote transformation, that is to say, our practice experience and The guidelines proposed by the central government are completely consistent. As mentioned above, although a number of tool companies have made significant progress, from the perspective of the whole industry, the transformation of most enterprises is far from enough, and it is necessary to catch up. The central leadership pointed out that the "Thirteenth Five-Year Plan" is the "last window period" for China's economic transformation, upgrading, restructuring, and transformation. Therefore, the vast number of tool enterprises should further understand and correctly judge the current situation, firmly grasp this rare opportunity for development, change their concepts, correct their mentality, eliminate all thoughts of waiting and waiting, and accelerate the process of transformation and upgrading without hesitation.

Our door handles are manufactured in high-grade material, with high performance of anti-rusting, which is ideal for both residential and commercial buildings. Including both tube door handles and solid door handles.

To ensure the quality of our door handles, we have strict quality control from material processing, polishing, assembly and packaging. Extensive experiences, mature technology and professional service allows us to meet the different needs of customers of different regions. Every product comes complete with mounting hardware. Special requirements and sizes are available. Please just feel free to contact us if you have any question. Our team is on call for 24/7 to provide the worry-free before/after-sale service.buildings.

Stainless Steel Solid Door Lever Handles

Stainless Steel Handles For Door ,Door Lever, Lever Handles Set, Solid Door Lever Handles

Leader Hardware Manufacturer Limited , https://www.leaderhardwarecn.com