Affected by the environmental storm at the national level, the market's expectation of the backward elimination of steel production capacity has increased. This was due to the strong rebound in the price of ** thread and bulk HRC prices last Thursday for several days. At the same time, with the rapid rise of the financial capital market, the spot market price of steel has also increased significantly in just three or four days. Merchants have followed suit and pushed up, and even some large steel traders in some regions are reluctant to sell and seal.

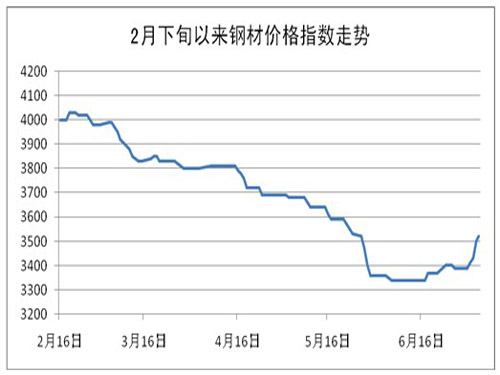

Affected by the environmental storm at the national level, the market's expectation of the backward elimination of steel production capacity has increased. This was due to the strong rebound in the price of ** thread and bulk HRC prices last Thursday for several days. At the same time, with the rapid rise of the financial capital market, the spot market price of steel has also increased significantly in just three or four days. Merchants have followed suit and pushed up, and even some large steel traders in some regions are reluctant to sell and seal. Recalling this round of steel price decline, it was characterized by sluggish demand, gloomy prices, and difficulties in shipping. Since late February of this year, it has taken more than four months. Taking the Shanghai market as an example, the rebar price went from a peak price of 3,890 yuan/ton in late February to a lowest point in early July of 3,330 yuan/ton, down by 560 yuan/ton, a decrease of nearly 15%. The price of hot coils from the highest price point in late February to 4270 yuan / ton, to the lowest point in early July 3320 yuan / ton, down 950 yuan / ton, a decrease of more than 22%.

Until last week, domestic steel market prices rebounded sharply, and prices in some regions and varieties rose by one hundred yuan. Some out of stock speculation soared 150 yuan / ton. However, judging from the market trading situation in the second half of the week, after the price was rapidly increased, the trading volume shrank sharply from the previous two days.

Obviously, in July, when steel demand was sluggish, steel prices could rebound sharply. This was first and foremost a policy stimulus. The State Council meeting proposed to complete the task of eliminating backward production capacity one year ahead of schedule. The NDRC requires all localities to clean up and inspect illegal production capacity of steel and other surplus industries. For violations, it is not allowed to approve, file, and provide land, environmental assessment, and credit support. The Ministry of Environmental Protection thoroughly inspects steel projects built or under construction in recent years. As a result, increasingly stringent environmental protection policies provide a rebound opportunity for steel prices.

At the same time, the strict handling of the two steel mills and their related persons in the Hebei region is an indication of the government's attitude and strength in implementing this environmental policy. Traders are optimistic about this and believe that this will change the operating structure at the bottom of the market, curb the continued expansion of crude steel production, and weaken the contradictory pattern of supply far beyond demand.

Second, social stocks continued to decline. Since late March, the domestic social inventory of major steel products has dropped for 16 consecutive weeks, a decrease of nearly 5.46 million tons, a decrease of more than 26%. As trader stocks are generally low, the demand for make-up stocks has also contributed to the recent rise in steel prices. According to the latest data, at present, the total inventory of steel products in major cities across the country is 16.3697 million tons, down 2.46% on a week-to-week basis, and is still in decline. At the same time, the inventory of key steel enterprises of China Iron and Steel Association has also declined. From the inventory cycle, the clearing of steel products is coming to an end, and the demand for supplementary materials has been enlarged.

Again, the steel mills saw a slight increase in production cuts. Due to the heavy price inversion of the current period, traders are in short supply of funds and their enthusiasm for ordering is not high. The pre-orders of steel mills were generally unsatisfactory and the losses were serious. Some steel mills chose to voluntarily reduce production to limit the sharp increase in in-plant inventory. In addition, tight liquidity is transmitted to the steel mills. Many small steel mills have increased financial pressure. Affected by the recent rise in raw material prices, they are forced to limit production and reduce production. This is reflected in the spot market as a reduction in the amount of steel plant resources .

In the end, raw material prices rose. Last week, foreign mineral prices rebounded again. At present, Australia's 62.5 taste powdered ore Qingdao Port has been quoted at 865 yuan/ton, with a single-week increase of more than 30 yuan/ton. At the same time, under the manipulation of speculators and reluctant sellers, the billet price has a shortage of market resources and the prices have rapidly increased, and have risen by nearly RMB 130/t in the second half of the week. The rebound in raw material prices stimulated the price increase in the finished material market and provided some support for pushing up prices.

It should be noted that the current demand for steel products does not show signs of significant growth. Downstream purchases still show signs of sluggish growth. Market transactions are dominated by traders. The decrease in inventories is mainly due to the fact that the order quantity of traders has continued to be low and the market has not arrived much. The output of steel mills has been at a high level. The overall oversupply situation has no substantive changes. The rise of policy stimulus alone has no major impact on the long-term trend of the market. If, in the short term, demand cannot be followed up effectively, the transaction will certainly fall back and steel prices may return to consolidation.

Stainless Steel Handrail Fittings

Stainless Steel Handrail Fittings,Wall Mounted Vertical Handrail Brackets,Stainless Steel Railing Fittings,Stairs Stainless Steel Handrail

Foshan Maysky Stainless Steel Co., Limited , https://www.mayskysteel.com